Have you ever wondered what would happen to your loved ones financially if you were no longer around? Life insurance is more than a financial product – it promises financial security for those who depend on you. In simple terms, life insurance is a policy that pays out a sum of money to your beneficiaries in the event of your passing. This ensures your loved ones have the financial means to carry on, settle outstanding obligations, and preserve their quality of life.

At MHG Wealth Management, we believe life insurance is a cornerstone of any sound financial plan, especially if you have a mortgage, children, or dependents who rely on you. With the right coverage, you’re not just protecting wealth; you’re protecting your family’s future.

Understanding Life Insurance

When considering life insurance, understanding how policies work and the different types available can help you make informed decisions tailored to your needs.

What Is Life Insurance?

Life insurance is a contract between you and an insurer, where you pay regular premiums in exchange for a lump-sum payout (the “death benefit”) to your beneficiaries upon your death. Understanding the differences, such as Universal life insurance vs whole life insurance, can help you choose the policy that best aligns with your financial goals and coverage needs. This coverage can ease financial stress during difficult times, helping with mortgage payments, daily expenses, or even funding future needs like education costs.

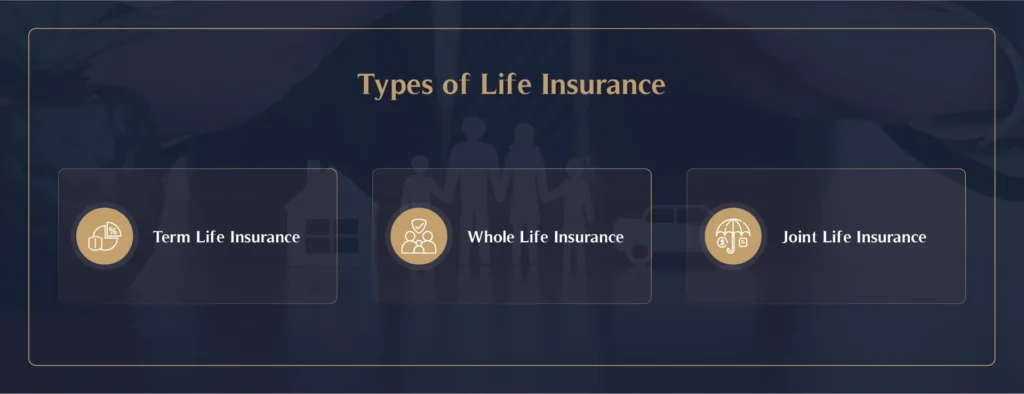

Types of Life Insurance

- Term Life Insurance: Imagine this as a safety net that’s put in place for a specific period, say 10, 20, or 30 years. During this time, if you were to pass away, the policy ensures that your loved ones receive a payout to cover pressing financial responsibilities like a mortgage or children’s education. Think of it as temporary but targeted protection—direct, cost-effective, and designed to provide peace of mind for a defined phase in life.

- Whole Life Insurance: This is like a lifelong financial anchor. It provides coverage that lasts your entire life while also growing in value over time. As you pay premiums, part of that payment builds up as “cash value” within the policy – like a small savings account within your insurance. This cash value can be accessed or borrowed against if you ever need extra funds. Whole life insurance isn’t just about leaving a legacy; it’s a financial resource that can support you while you’re living and leave a lasting benefit to your heirs.

- Joint Life Insurance: For couples, joint life insurance is like a shared safety net. This policy covers two people under one plan, usually a married couple, and can pay out either after the first partner’s death (first-to-die) or after both have passed away (second-to-die). This flexibility means it can adapt to your family’s needs. For couples aiming to secure their shared financial future, it’s a practical, often more affordable way to ensure both parties are protected, with the policy structure adjusted to suit your specific goals.

How Life Insurance Works

Understanding how life insurance works can empower you to make decisions that benefit your family in the long term.

- The Policy Process

Getting life insurance starts with selecting a policy that suits your financial needs and applying for coverage. Insurers assess factors such as age, health, and lifestyle to determine eligibility and premium rates. Working with a financial advisor can simplify this process and ensure you get the right level of cover. - Premium Payments

Premiums are the regular payments you make to keep the policy active. They can vary based on coverage level, type, and your health profile. Generally, premiums for term life policies are lower than for whole life, making them attractive for those with temporary needs or budget considerations. - Beneficiaries and Death Benefits

Beneficiaries are the individuals you designate to receive the policy’s death benefit. This money can serve various purposes, from settling debts and funding education to covering daily living expenses.

Types of Life Insurance Policies

- Term Life Insurance

Term policies provide straightforward coverage with an affordable premium, offering peace of mind for those with specific financial obligations like a mortgage or family support. If you pass away during the policy term, your beneficiaries receive the payout; if you outlive the policy, coverage ends unless you choose to renew or convert it. - Whole Life Insurance

Whole life insurance provides lifetime coverage, often with higher premiums due to its cash value component. This cash value grows over time and can be borrowed against, providing a financial cushion if needed. Whole life insurance is ideal for those seeking lifelong protection and a built-in savings component. - Joint Life Insurance Policies

Joint life insurance covers two people under a single policy. It’s often chosen by couples, as it can be more cost-effective than individual policies. With the option of either first-to-die or second-to-die payouts, joint life insurance offers flexibility in planning for a partner’s future security.

Life Insurance and Critical Illness Policies

While life insurance covers your beneficiaries if you pass away, critical illness insurance provides financial support if you’re diagnosed with a severe illness covered by the policy. Having both life and critical illness insurance ensures you’re protected during life’s unexpected health challenges, while also securing a financial legacy for your loved ones.

Purchasing Life Insurance

Steps to Buy Life Insurance

Buying life insurance involves identifying your needs, choosing a suitable policy, and comparing quotes. A financial advisor can help you assess how much coverage you need based on factors like income, debts, and family financial planning requirements.

Comparing Life Insurance Quotes

Insurance rates can vary widely. By comparing quotes, you can secure the most cost-effective premium for your chosen coverage. Using an insurance calculator also helps you understand potential costs and coverage options based on your age, health, and financial goals.

Life Insurance and Financial Planning

Life insurance can support various aspects of your financial plan.

Here are some ways it can help:

- Life Insurance and Mortgage Requirements

Some mortgage lenders require life insurance to ensure your loan will be repaid if something happens to you. Term life insurance can fulfil this need, providing protection for your home and your loved ones. - Life Insurance as a Savings Plan

Whole life policies can act as a savings plan due to their cash value component. Over time, this value grows and can be used for other purposes, like supplementing retirement income. - Impact on Inheritance Tax

In the UK, life insurance can help reduce inheritance tax. Placing a policy in trust ensures that the payout goes directly to beneficiaries, bypassing inheritance tax and maximising the financial legacy you leave.

Conclusion

Life insurance is one of the most important steps in a solid financial plan. It provides stability, peace of mind, and security, ensuring your loved ones have financial support even in your absence. With options ranging from term and whole life insurance to joint and critical illness coverage, you can build a plan that fits your family’s unique needs.

At MHG Wealth, our advisors specialise in helping you choose the right life insurance coverage to support your family, safeguard your assets, and protect your future. Contact us today to speak with an advisor about finding a life insurance policy that aligns with your goals and offers you true financial peace of mind.

FAQS

Can You Have More Than One Life Insurance Policy?

Yes, multiple policies are allowed, often used to address different financial needs.

Do You Need Life Insurance for a Mortgage?

Some lenders require it, but even if they don’t, it’s wise to ensure your family can continue living in the home if something happens to you

What Does Life Insurance Cover?

Life insurance generally covers death due to natural causes, illness, or accident, though specific policies may vary.

How Long Should I Get Life Insurance For?

This depends on your financial obligations and family needs. Term life policies are often chosen for specific timeframes, while whole life provides permanent coverage.

How much life insurance do I need?

The amount of coverage you need depends on your financial obligations and your family’s needs. A financial advisor can help you determine the right amount.

How do I choose a life insurance policy?

Consider factors like your age, health, budget, and coverage needs. Compare quotes from different insurers to find the best policy for you.

Can I cancel my life insurance policy?

Yes, you can usually cancel your policy at any time. You may receive a cash value refund or surrender value, depending on the policy type.