UK interest rates are an important part of finance. When you borrow money, the amount you repay depends on the interest rate and any extra fees. This also applies to savings accounts where you can earn interest.

It’s essential to understand interest rates in personal finance in order to have a successful financial future. This guide explores what interest rate are, their role in financial transactions, how to find the best interest rates and all the latest trends.

Key takeaways:

- The interest rate is the fee you pay for borrowing, or what you earn for saving

- The Bank of England has kept interest rates high since 2021

- You can find great deals for borrowing and saving if you work with financial advisers

Understanding interest rates

Borrowing money often comes at a price. The fee you pay for borrowing it is the interest. If you do this through a loan or credit card, the interest is usually shown as an annual percentage.

When you save money, the bank or building society you are with is borrowing your money, so it pays you interest in return.

The Bank Rate – sometimes known as the Bank of England Base Rate, is set by the Monetary Policy Committee and government, in order to try and keep inflation low and stable. This rate sets the amount of interest paid to commercial banks, and that influences what they charge customers for lending, and what they pay you for saving.

If the Bank Rate increases, the cost of borrowing goes up and savings interest also increases.

If the Bank Rate decreases, the opposite happens.

Interest rates can also have a big impact on investments – including borrowing costs and ROI.

Types of interest rates

It is important to understand the difference between fixed and variable interest rates if you want to borrow money. Whether you’re looking for a new mortgage, a personal loan or a credit card, knowing the difference can help you save money.

- Fixed rate – The interest rate will not change on your mortgage or loan. Although a fixed rate is typically higher than a variable rate, you will avoid the uncertainty of whether the rate could rise and end up costing you more than you budgeted for. Fixed rate is very beneficial when interest rates are relatively low.

- Variable rate – These interest rates can go up and down and are often influenced by Bank Rate changes. When market interest rates are low, you will benefit from low borrowing costs. But if rates increase, you will pay more.

Interest rates in the UK

Current trends in interest rates

The Bank of England began raising Interest rates in 2021 to try and reduce inflation caused by COVID-19 and Russia’s invasion of Ukraine.

In August 2024, the interest rate was reduced from 5.25% to 5%. Three months later, the interest rate was lowered from 5% to 4.75%, and the next announcement is due in February. Although experts predict the rate may drop further, it is expected to remain high.

Mortgage interest rates

Mortgage interest rates are currently high due to the current interest rate trends. Fixed rate mortgages have been rising in price throughout January 2025. However, borrowers may still be advised it is in their interests to fix a new deal, as the alternative – defaulting to a standard variable rate – is likely to be more expensive.

Despite this news, it’s a good idea to speak to expert financial advisers, who may be party to deals that aren’t easy to find.

Personal loan interest rates

If you are considering borrowing a lump sum to help you pay for home improvements or a new car, you can borrow through an unsecured personal loan. Typically, these loans allow you to borrow from £1,000 to £50,000 over periods of one to 10 years.

- £5,000 loans over three years – the best deals are 7.2%

- £10,000 loans over five years – the lowest deals are 5.9%

- £15,000 loans over five years – again, the lowest are 5.9%

- £25,000 loans over five years – the lowest deals are again currently 5.9%

Savings account interest rates

Make sure your savings account aligns with your saving goals. A financial adviser can help with this. And of course, with savings accounts, the higher the rate, the better.

- Fixed rate savings accounts – good for you if you are happy to lock your money away to get a better rate. Currently the top fixed rate sits at 4.77%

- Easy access savings accounts – let you withdraw money when you need it. The best rate available is 5.12 – but if you withdraw any within a month, that rate drops to 3.25%

- Regular savings account – you deposit a set amount of money every month. Interest rates can currently go as high as 7%

Finding the best interest rates

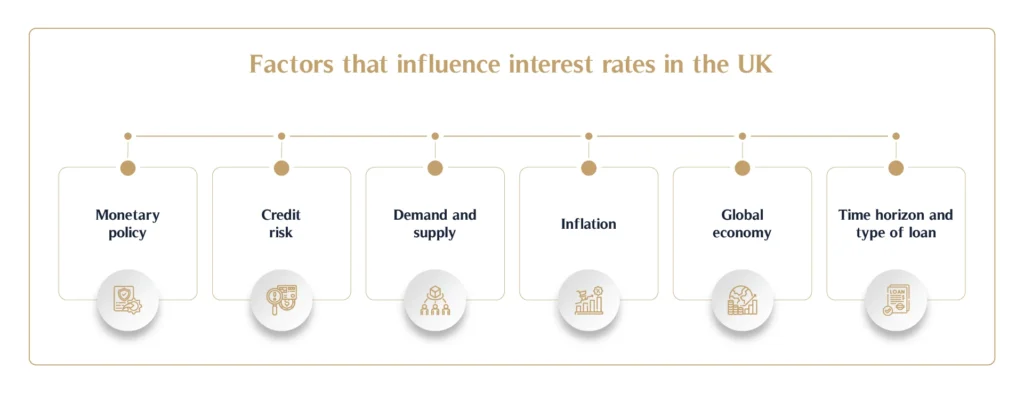

Factors that influence interest rates in the UK

- Monetary policy – Central banks influence interest rates by managing the money supply

- Credit risk – The creditworthiness of borrowers has an impact on interest rates

- Demand and supply – Interest rates go up as demand exceeds supply and vice versa

- Inflation – If prices rise, lenders will demand higher rates

- Global economy – International trends also affect interest rates

- Time horizon and type of loan – The longer the term and the riskier the loan, the higher the rate

How to secure the best mortgage interest rates

- Improve your credit score – Reduce debts, correct credit report inaccuracies and limit new credit card applications

- Save for a larger deposit – Usually, the larger your deposit, the lower your interest rate

- Compare mortgage deals – Ensure you’re getting the best deal out there

- Fixed vs variable rates – Choose which best matches your financial situation

The best savings account interest rates available

Currently, the best interest rates are all over 4%.

- Instant access – 4.75%

- One-year fixed rate – 4.77%

- Two-year fixed rate – 4.71%

- Three-year fixed rate – 4.63%

- Four-year fixed rate – 4.51%

- Five-year fixed rate – 4.8%

Whether it’s mortgages, loans, credit cards or savings accounts, interest rates affect everybody. They have such a huge impact on the economy. That’s why it’s important to stay updated on interest rate changes, and be informed about their implications. This can be done much easier if you have experienced financial advisers on board, so get in touch with the MHG Wealth Management today.