The quest for stable, predictable returns has driven investors to explore alternative fixed-income options. These investments provide opportunities beyond traditional bonds or savings accounts, offering both higher yields and greater portfolio diversification.

Among the standout options in this space are private credit and peer-to-peer (P2P) lending, two distinct yet compelling avenues for generating consistent returns.

Private credit involves lending by non-bank institutions to businesses or individuals, often through customised arrangements. P2P lending, on the other hand, uses online platforms to connect individual investors directly with borrowers, democratising access to credit markets.

This guide delves into the intricacies of both private credit and P2P lending, highlighting their advantages, risks, and suitability for investors. By comparing these alternatives, we aim to empower you to make informed decisions that align with your financial goals.

What is Private Credit?

Private credit refers to loans issued by private institutions, such as investment funds or private lenders, to businesses or individuals. Unlike traditional bank loans, private credit deals are highly customisable and cater to specific borrower needs, providing flexibility that sets them apart from public fixed-income instruments.

Types of Private Credit Investments

- Direct Lending: These are loans issued directly to middle-market businesses, often to fund growth, acquisitions, or operations.

- Mezzanine Financing: A hybrid model that blends debt and equity, mezzanine loans offer higher yields but come with increased risk.

- Distressed Debt: Investments in companies facing financial difficulties, offering high returns for investors willing to assume greater risk.

Advantages of Private Credit

- Higher Yields: With returns typically surpassing traditional bonds, private credit offers investors attractive compensation for taking on additional risk.

- Customisable Terms: Lenders and borrowers negotiate terms tailored to their unique objectives, making these loans more flexible than standard bank-issued debt.

- Portfolio Diversification: Private credit investments provide exposure to non-traditional markets, helping reduce reliance on volatile public markets.

Risks of Private Credit

- Illiquidity: Investments in private credit often require locking in funds for several years, limiting short-term access to capital.

- Credit Risk: Borrowers may fail to meet repayment obligations, especially in volatile economic conditions.

- Regulatory Complexity: Private credit operates within a complex regulatory framework that varies by region, adding another layer of risk for investors.

What is Peer-to-Peer Lending?

Peer-to-peer lending, commonly known as P2P lending, is a financial innovation that connects individual lenders with borrowers through online platforms. This approach bypasses traditional banking systems, allowing investors to fund loans directly and earn competitive returns.

How Peer-to-Peer Lending Works

- Borrowers seek loans on P2P platforms for purposes such as personal expenses, business growth, or debt consolidation.

- Lenders fund these loans in exchange for interest payments, with platforms facilitating the connection.

- Repayments are made over time, providing lenders with both principal and interest income.

Examples in Dubai

Emerging P2P platforms are addressing the financing gap for startups and SMEs in the UAE.

International platforms like Funding Circle and LendingClub are influencing local market trends by offering models for growth.

Advantages of P2P Lending

- Accessibility: Investors can start with small amounts, making P2P lending ideal for retail investors.

- Higher Yields: Returns often surpass those of traditional savings accounts or bonds, making it an attractive fixed-income alternative.

- Diversification: By investing in multiple loans across sectors, lenders can spread risk and reduce exposure to any single borrower.

Risks of P2P Lending

- Borrower Defaults: Platforms may not always secure loans with collateral, increasing the risk of loss.

- Platform Reliability: Not all platforms are created equal; due diligence is crucial to avoid unreliable providers.

- Regulatory Oversight: As an emerging sector in Dubai, P2P lending in Dubai is still evolving, which may expose investors to regulatory gaps.

Private Credit vs. Peer-to-Peer Lending: Key Differences

When comparing private credit and peer-to-peer (P2P) lending, the differences are striking. Both are powerful fixed-income alternatives, yet they cater to different types of investors and offer unique benefits and risks. Understanding these differences is crucial for making informed investment decisions.

Here are the key differences between private credit and peer-to-peer (P2P) lending:

-

Capital Requirements

Private credit is generally suited for experienced investors or institutions with access to significant capital. These investments often involve large-scale financing for middle-market businesses, infrastructure projects, or distressed debt acquisitions. Due to the high entry thresholds, private credit is often the domain of high-net-worth individuals (HNWIs) or institutional investors.

In contrast, P2P lending democratises access to fixed-income opportunities. By leveraging online platforms, retail investors can participate with minimal capital, sometimes as little as a few hundred dollars. This accessibility makes P2P lending an appealing entry point for those exploring alternative investments without the financial burden of private credit’s high requirements.

-

Target Audience

Private credit is tailored to sophisticated investors seeking structured and customised financing solutions. It’s a preferred choice for institutional investors, pension funds, or HNWIs aiming to diversify portfolios with investments offering consistent, high-yield returns.

On the other hand, P2P lending caters to a broader audience, including retail investors eager to earn higher interest rates compared to traditional savings accounts. It also appeals to smaller-scale investors who value the ability to allocate funds across a diverse range of borrowers.

-

Risk and Return Profiles

Private credit is generally considered a lower-risk option in the alternative fixed-income space due to the rigorous due diligence and structured nature of these investments. Loans are often secured, mitigating the risk of borrower default. Returns, while competitive, are steady rather than exponential, aligning well with long-term financial strategies.

P2P lending offers the allure of higher potential returns but comes with a greater degree of risk. Borrower defaults, platform reliability, and limited regulation contribute to its volatility. For investors willing to navigate these risks, P2P lending provides opportunities to outperform traditional fixed-income returns.

-

Regulatory Landscape

Private credit operates within well-established legal frameworks, providing a high level of security and transparency for investors. This robust regulatory oversight ensures consistent standards and reduces uncertainty.

P2P lending, particularly in Dubai, remains an evolving sector. While fintech platforms in the region are expanding, the regulatory environment is still catching up. Investors must approach P2P lending with caution, conducting thorough due diligence on platforms and adhering to local financial guidelines.

Opportunities in Dubai’s Fixed-Income Market

Dubai is quickly establishing itself as a hub for alternative fixed-income investments. Both private credit and P2P lending are gaining momentum, driven by the city’s growing economy, expanding fintech ecosystem, and supportive government initiatives.

Private Credit in Dubai

Private credit in Dubai is primarily focused on SME lending and infrastructure development, aligning with the government’s commitment to economic diversification. Initiatives like Dubai Vision 2040 have created an unprecedented demand for private financing in sectors such as logistics, healthcare, and renewable energy.

Moreover, private credit funds are increasingly tapping into Dubai’s vibrant real estate market, offering mezzanine financing for luxury developments and commercial projects. With a stable regulatory environment and strong economic fundamentals, private credit presents a lucrative opportunity for institutional investors and HNWIs seeking long-term growth.

Peer-to-Peer Lending in Dubai

Dubai’s fintech revolution has positioned P2P lending as a key player in the alternative financing market. P2P platforms are bridging the gap for borrowers who may lack access to traditional bank loans, such as startups, freelancers, and individuals.

For investors, P2P lending in Dubai offers exposure to a diverse borrower base, ranging from entrepreneurs to consumers. The city’s growing population of expats and SMEs ensures a steady demand for credit, creating a dynamic environment for P2P investments. However, as the sector matures, platform reliability and borrower screening remain critical considerations.

Private Peer-to-Peer Lending

For HNWIs seeking a hybrid approach, private peer-to-peer lending combines the advantages of customised credit arrangements with the efficiency of digital platforms. This model allows HNWIs to lend directly to borrowers under customised terms, offering both control and the potential for higher returns.

As Dubai’s regulatory framework evolves, opportunities for private P2P lending are expected to expand, further enhancing the city’s position as a global hub for innovative financing solutions.

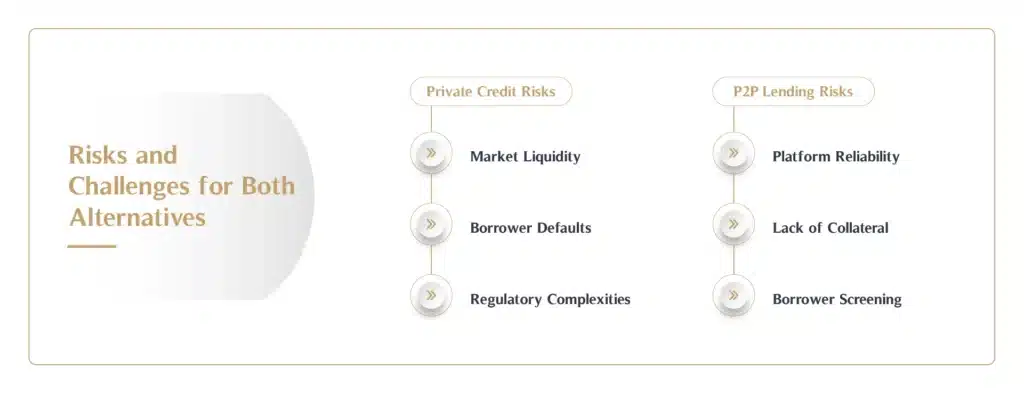

Risks and Challenges for Both Alternatives

Investing in alternative fixed-income options such as private credit and peer-to-peer (P2P) lending comes with its share of risks. Understanding these challenges is vital to safeguarding investments and maximising returns.

Here’s a closer look at the potential pitfalls associated with each:

Private Credit Risks

- Market Liquidity:

Private credit investments are inherently illiquid. Unlike publicly traded securities, these loans cannot be easily sold or exited before maturity. Investors must be prepared to tie up their capital for extended periods, which could be challenging in volatile economic conditions. - Borrower Defaults:

Despite rigorous due diligence, private credit remains susceptible to borrower defaults. Businesses facing economic downturns or operational issues may struggle to meet repayment obligations, posing risks to lenders. The impact of defaults can be particularly pronounced for investments in distressed debt or mezzanine financing. - Regulatory Complexities:

Private credit operates within a complex legal framework that varies across jurisdictions. Investors must navigate compliance issues, from understanding local regulations to ensuring contractual safeguards. Missteps in this area can lead to legal disputes or financial losses.

P2P Lending Risks

- Platform Reliability:

The viability of P2P lending relies heavily on the platform facilitating the transactions. The risk of platform mismanagement, fraud, or even bankruptcy can jeopardise investor funds. Conducting thorough research into platform credibility is critical. - Lack of Collateral:

Many P2P loans are unsecured, leaving investors exposed in cases of borrower default. Without collateral as a safety net, the recovery of funds becomes significantly more challenging, especially in less mature markets. - Borrower Screening:

P2P lending platforms vary in the rigour of their borrower assessment processes. Weak or insufficient screening can result in higher default rates, directly impacting returns. Investors must carefully evaluate the platform’s risk management protocols before committing funds.

Regulatory Considerations

Both private credit and P2P lending are influenced by Dubai’s evolving financial regulations. The government is working to modernise frameworks for alternative finance, but investors must stay informed about these developments. For private credit, adherence to contractual and compliance standards is essential. Meanwhile, P2P investors should monitor regulatory updates concerning platform operations and borrower protections.

How to Choose the Right Fixed-Income Alternative

Selecting between private credit and P2P lending, or choosing to invest in both, requires a strategic approach.

Here’s how to determine the right path for your financial goals:

-

Portfolio Diversification

Alternative fixed-income investments offer diversification beyond traditional assets like stocks or bonds. To balance risk and reward, consider allocating funds across both private credit and P2P lending. For example:

- Use private credit for long-term, stable income.

- Allocate smaller amounts to P2P lending for higher-yield, shorter-term returns.

This blended approach can shield your portfolio from market volatility while tapping into the unique benefits of each investment type.

-

Due Diligence

Thorough research is critical before committing to either option:

- For Private Credit: Assess the track record and expertise of fund managers. Understand their approach to risk management and how they navigate market uncertainties.

- For P2P Lending: Investigate platform reputation, borrower screening processes, and recovery mechanisms. Focus on platforms with transparent operations and a proven history of consistent returns.

Strong due diligence reduces exposure to unnecessary risks and increases the likelihood of achieving your desired outcomes.

-

Risk Appetite

Your risk tolerance plays a crucial role in deciding which alternative to pursue:

- If you prioritise steady, predictable returns and can commit capital for extended periods, private credit may align better with your goals.

- If you’re open to higher risk for the possibility of greater rewards, P2P lending offers opportunities to earn competitive returns through diversified borrower portfolios.

Ultimately, the right choice depends on your financial objectives, investment horizon, and willingness to manage potential challenges.

Conclusion

Private credit and P2P lending offer unique advantages within the fixed-income space, catering to different investor profiles and goals. Private credit provides structured, high-capital opportunities with managed risks, while P2P lending democratises investing, allowing retail investors to access competitive returns.

Dubai’s dynamic financial landscape provides fertile ground for both options, driven by economic growth and fintech innovation. Whether you prefer the tailored flexibility of private credit or the accessibility of P2P lending, aligning your choice with your financial goals and risk tolerance is key.

At MHG Wealth, we help clients navigate the complexities of alternative investments by tailoring strategies that suit their individual needs. Connect with us today to know how these fixed-income alternatives can level up your portfolio.