There are many different types of life insurance, and universal life insurance and whole life insurance are two popular choices. Although there are similarities between the two, they are not the same.

Universal life insurance is a permanent life insurance, with a cash value element and lifetime coverage.

Whole life insurance is also a permanent life insurance. It pays a tax-free death benefit and also contains a savings component, in which cash value may accumulate.

It’s important to understand different life insurance options, and expert financial advisers can help guide you through this often complex world.

In this guide, we’ll evaluate if universal life insurance is suitable for you, we’ll help you to understand whole life insurance, we’ll examine universal life insurance, and we’ll compare the two, to help you decide which would suit you best.

Key Takeaways:

- Universal life insurance and whole life insurance are both types of permanent life insurance

- Universal life insurance offers more flexibility

- Whole life insurance has guaranteed cash value

Understanding Whole Life Insurance

If you have whole life (WL) insurance, it lasts your lifetime, and when you die, whole of life cover pays out a lump sum to your beneficiaries. This is different to term life insurance, which guarantees a death benefit pay-out within a fixed period.

Benefits of whole life insurance

- Guaranteed death benefit

- Fixed premiums

- Guaranteed cash value that you can use while still alive

- Guaranteed earnings

- Can never become underfunded

Comparison with universal life insurance

- May allow you to change the level of death benefit

- Flexible premiums

- Potential cash value you can use while still alive

- Interest rates may change

- May become underfunded and lapse

One of the most alluring features of whole life insurance is the combination of coverage and savings provided. Your insurance company places part of your premium payments into a high-interest bank account, or investment account. Your cash value accumulation increases every time you make a premium payment.

Whole life insurance is an ideal policy for helping you to achieve your long-term financial goals.

Exploring Universal Life Insurance

Universal life insurance, also known as adjustable life insurance, is more flexible. With this insurance, you have the option to adjust:

- Your premiums – This helps you cope with income variations or changes in financial circumstances

- Your death benefits – A universal life policy is helpful as life events change your circumstances, for example, marriage, or home ownership

- Your cash value accumulation – The link to prevailing interest rates gives you the chance to participate in financial markets and can help provide long-term growth – but remember that interest rates can go down as well as up

It’s this flexibility that makes universal life insurance attractive to people with changing financial circumstances, and/or looking for a customisable approach to their life insurance.

What is indexed universal life insurance?

Indexed universal life (IUL) insurance is a specific type of universal life insurance, providing a cash value component as well as death benefit.

The money in your cash value account can earn you interest, by tracking a stock market index chosen by the insurer. And if your policy also has a fixed-rate account, you can decide how much goes into each account.

Bear in mind that indexed universal life insurance policies cap how much money you can accumulate – often at less than 100%. Also, they are based on a potentially volatile equity index.

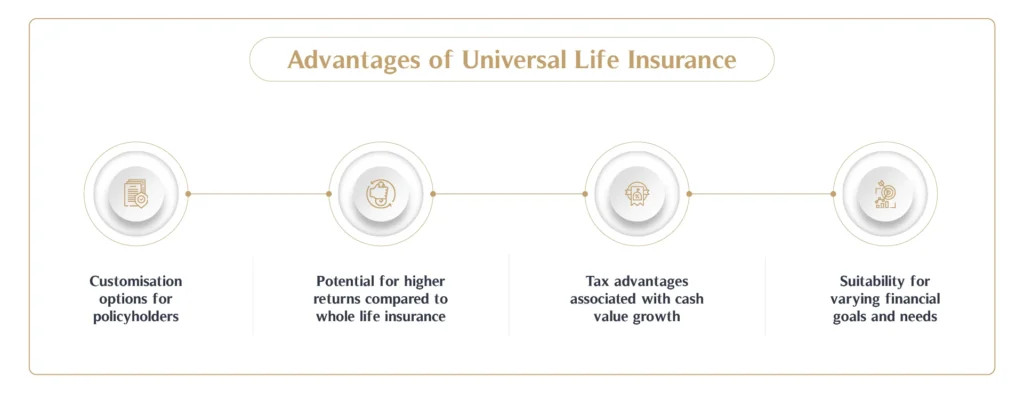

Advantages of Universal Life Insurance

Customisation options for policyholders

You can change the size and frequency of your payments, which can prove very useful if you’re going through financially testing times. And you may also be able to increase the death benefit if you require more – but you’ll need to pass a life insurance medical exam to qualify. You can decrease the death benefit too, providing you’ve held the policy for a few years.

Potential for higher returns compared to whole life insurance

As indexed universal life insurance is linked to a stock market index, you could potentially get a higher return compared to whole life insurance. Variable universal life insurance lets you invest your cash value component in stocks, bonds and mutual funds, which can also provide high returns.

Tax advantages associated with cash value growth

Cash value growth is tax-deferred, so you don’t have to pay taxes on the gains as they accumulate, or the interest that you earn as it grows, either.

Suitability for varying financial goals and needs

If you’re seeking flexibility in your life insurance, or you feel your needs may change through the years, universal life insurance is a great choice, because of its adaptability. Life can be unpredictable, after all.

Summary

So we can see that despite their similarities, universal life insurance and whole life insurance are different. Both allow you to borrow against or withdraw the cash value. However, universal life insurance gives you flexible premiums and death benefits, while whole life insurance offers consistent premiums, that are usually higher than universal life premiums.

Before you choose a life insurance policy, it’s important to assess your personal financial situations and goals. Everyone is different, with unique needs, so you need to weigh up the advantages of life insurance policies, and obviously, the disadvantages too.

Even if you think you know which is the one for you, it’s a good idea to speak to a qualified financial adviser, then you can get peace of mind you made the right choice for your money.

For the best personalised advice, get in touch with MHG Wealth to see how we can give you the confidence to plan for your financial future.